Receiving a life insurance payout can be emotionally overwhelming — it often comes after the loss of a loved one. But handled wisely, that money can offer lasting financial stability and peace of mind. Whether it’s a small benefit or a large sum, making the right choices with life insurance money ensures the funds serve your future goals and honor your loved one’s legacy.

1. Pause and Plan Before Making Decisions

The first and most important step: don’t rush.

After receiving a life insurance payout, it’s normal to feel pressure to make quick financial decisions — especially if bills are due. But most financial advisors recommend waiting at least a few weeks or months to think through your goals.

Use this time to:

-

Pay for immediate essentials (funeral costs, monthly bills)

-

Avoid large or emotional purchases

-

Meet with a certified financial planner (CFP) to outline a plan

Taking a short pause helps you make thoughtful, not impulsive, decisions.

2. Cover Immediate Financial Needs

If you’re the primary beneficiary, your first priority is stability. Consider using a portion of the payout to cover:

-

Funeral or memorial expenses

-

Outstanding medical bills

-

Mortgage or rent payments

-

Everyday expenses, such as groceries, utilities, and car payments

This ensures that life’s essentials are covered while you rebuild your financial footing.

3. Pay Off High-Interest Debt

High-interest debt — especially credit cards or personal loans — can drain your finances over time.

Using part of the life insurance money to eliminate these debts can:

-

Free up monthly income

-

Improve your credit score

-

Reduce financial stress

Start by paying off the highest-interest balances first, then work your way down.

4. Build or Replenish an Emergency Fund

Life insurance money can serve as a safety net. Ideally, keep three to six months’ worth of expenses in a liquid account (such as a high-yield savings account).

This fund provides financial security if you face job loss, medical emergencies, or unexpected costs in the future.

5. Invest for Long-Term Growth

Once immediate needs are handled, consider investing part of the funds for future goals. Options may include:

-

Retirement accounts (IRA, 401(k))

-

Mutual funds or ETFs for steady long-term growth

-

529 college savings plans if you have children

Diversifying your investments helps the money grow while protecting it from inflation.

If you’re unfamiliar with investing, a fee-only financial advisor can help design a portfolio that matches your risk tolerance and goals.

6. Secure Your Home and Lifestyle

If the policyholder was a financial contributor, you might use the payout to pay off or reduce your mortgage, helping you stay in your home long-term.

Other smart uses include:

-

Paying off a car loan

-

Making necessary home repairs or improvements

-

Covering future property taxes or insurance

These steps help maintain stability and prevent future financial strain.

7. Continue the Legacy

Life insurance money can also be a way to honor your loved one’s memory.

You might choose to:

-

Donate a portion to a meaningful charity or cause

-

Set up a scholarship fund in their name

-

Create a trust fund for children or grandchildren

These gestures provide emotional healing while creating a lasting impact.

8. Be Strategic About Taxes and Payout Options

Generally, life insurance payouts are not taxable at the federal level. However, if the money is held in an interest-bearing account or you receive it in installments, the earned interest can be taxed.

You can usually choose between:

-

Lump-sum payment (most common)

-

Annuity or installment payments, which provide steady income over time

Talk with a financial or tax advisor to decide which option aligns with your goals.

9. Protect the Remaining Funds

Once you’ve made a plan, safeguard the remaining money:

-

Use FDIC-insured bank accounts for short-term storage

-

Keep investments with reputable financial institutions

-

Avoid pressure from anyone promoting “quick investment opportunities” or high-risk ventures

A trustworthy advisor should be transparent about fees and focused on your best interests — not commissions.

10. Create or Update Your Own Life Insurance Plan

Finally, if you don’t already have your own life insurance policy, now is the time to get one. The experience of managing a payout can highlight how crucial coverage is for your own loved ones.

Consider term life insurance for affordability or whole life insurance for lifelong protection and potential cash value growth.

Final Thoughts

Life insurance money isn’t just a financial benefit — it’s a gift meant to protect your future.

The best way to use it is to:

-

Secure your immediate needs

-

Eliminate debt

-

Build savings and invest wisely

-

Honor your loved one’s memory through stability and growth

Handled thoughtfully, this money can provide both peace of mind and lasting financial independence — ensuring your loved one’s support continues to make a difference for years to come.

Life insurance money can help in many ways. It is important to use it wisely. The money can support your family after you are gone.

Pay Off Debts

First, you should pay off any debts. This includes home loans, car loans, and credit cards. Paying off debt can reduce stress. It can also save money on interest. Your family will feel more secure.

Cover Living Expenses

Next, use the money to cover daily living expenses. This includes rent, utilities, and groceries. It helps to keep life normal for your loved ones. They will not have to worry about bills.

:max_bytes(150000):strip_icc()/How-can-i-borrow-money-my-life-insurance-policy_final-fa1474645da94b368bb3f5452392b0c0.png)

Credit: www.investopedia.com

Save for Education

Education is very important. You can use the money to save for your children's education. College can be expensive. Saving now can help pay for tuition, books, and other costs. It will give your children a good start in life.

Invest Wisely

Investing the money can help it grow. You can invest in stocks, bonds, or mutual funds. It is a good idea to talk to a financial advisor. They can help you make smart choices. Investing can provide long-term financial security.

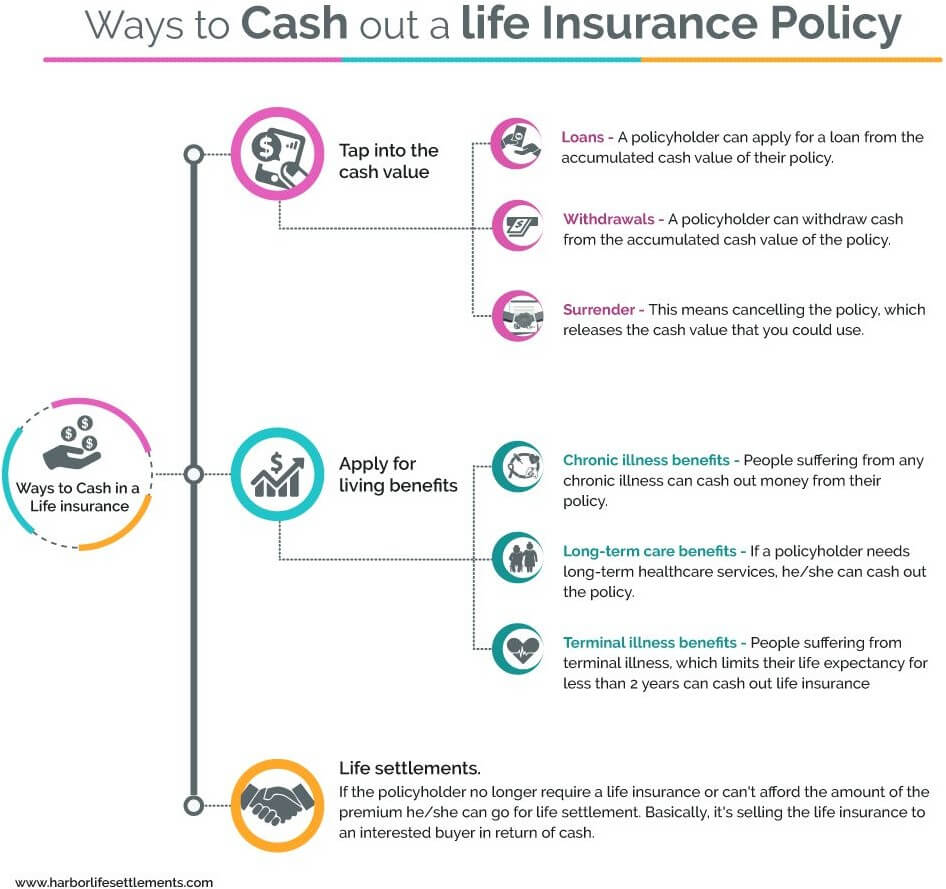

Credit: www.harborlifesettlements.com

Emergency Fund

Having an emergency fund is important. It can cover unexpected expenses. This includes medical bills or car repairs. An emergency fund can give peace of mind. It is good to have money set aside for a rainy day.

Charity Donations

Some people like to donate to charity. You can use life insurance money to support causes you care about. This can make a big difference. It can help others in need. Giving to charity can also be a way to honor your memory.

Home Improvements

Using the money for home improvements can be a good idea. It can increase the value of your home. It can also make your home more comfortable. This can be a good use of life insurance money.

Plan for Retirement

Retirement planning is important. You can use the money to save for retirement. This can help ensure a comfortable future. It is never too early to start saving for retirement.

Seek Professional Advice

It is always a good idea to seek professional advice. Financial advisors can help you make the best decisions. They can help you plan and manage your money. This can ensure that the money is used wisely.

Frequently Asked Questions

What Can Life Insurance Money Be Used For?

Life insurance money can be used for debts, education, or savings.

Can Life Insurance Money Be Invested?

Yes, you can invest life insurance money in stocks, bonds, or real estate.

Is Life Insurance Payout Taxable?

Life insurance payouts are usually not taxable. Check local laws.

Can Life Insurance Money Be Used For Retirement?

Yes, life insurance money can support your retirement plans.

Conclusion

Using life insurance money wisely is very important. It can help pay off debts, cover living expenses, save for education, and invest. It can also provide an emergency fund, allow for charity donations, and fund home improvements. Planning for retirement is also important. Always seek professional advice. This can help ensure a secure future for your loved ones.

{kind=link}

0 Comments